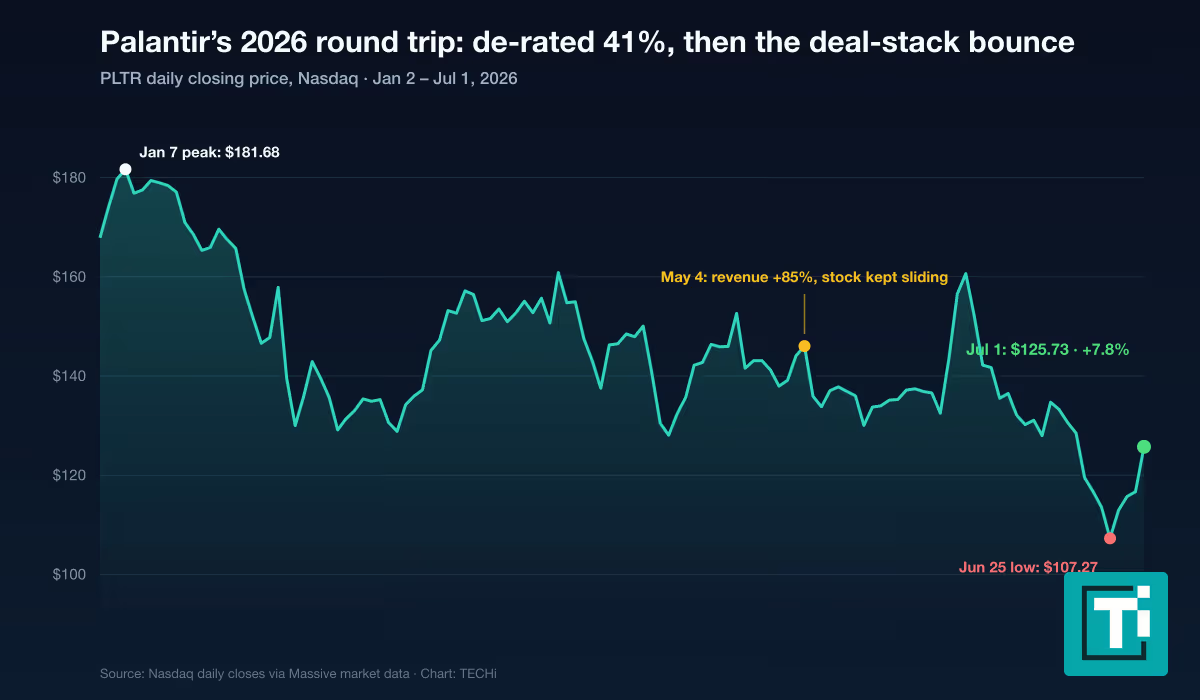

Palantir Technologies closed at $125.73 on Wednesday, July 1, 2026 — up 7.8% in a session that added roughly $21.7 billion to its market value on 57 million shares of volume. The proximate cause was a partnership: Palantir and NVIDIA are rolling out an engine for running NVIDIA’s AI models inside sovereign, secured environments, and the market treated it as a coronation.

The line every headline carried was “NVIDIA deal.” The line that matters more is this one: even after its best day in months, Palantir stock is still down about 25% for 2026 — a year in which the company reported the fastest revenue growth in its history and raised guidance twice. The stock spent five months getting cheaper while the business got better.

That gap is what July 1 was really about. Nothing that was announced last week carries a large disclosed dollar figure. What the rally repriced was positioning — and it happened on the same day a Bloomberg report about Meta’s cloud ambitions was tearing double-digit percentages off CoreWeave, Nebius and the rest of the GPU-rental complex. In one session, the AI trade picked sides: the layer that deploys AI in places hyperscalers cannot reach beat the layer that rents the chips.

Article Brief

Key Takeaways

5 Points30s Read

- The movePalantir closed July 1 at $125.73, up 7.8% — roughly $21.7 billion of market value added in one session, while much of the AI-infrastructure complex sold off.

- The triggerA deployment engine for NVIDIA Nemotron models in sovereign environments, capping nine days that also delivered the Army NGC2 data-layer baseline, a Zeta Global partnership and expanded Surf Air deals.

- The honest mathEvery dollar figure disclosed across the week totals well under 1% of the repricing. The market paid for positioning, not bookings.

- The contextPLTR is still down about 25% in 2026 — a 41% peak-to-trough de-rating that happened while revenue growth accelerated to 85%, its fastest ever.

- What settles itThe July NGC2 division-scale validation and the early-August Q2 report, where guidance calls for $1.797–1.801 billion in revenue.

The week Palantir stacked its story

The rally looks like a one-day event. It was actually the market clearing a backlog of six announcements in nine days.

On June 22, the U.S. Army set the common data layer baseline for Next Generation Command and Control, its highest-priority modernization program, with Palantir Foundry as the cloud data layer. On June 23, Zeta Global said it would rearchitect its Data Cloud on Foundry, projecting the partnership could drive more than $100 million in annual revenue over a multi-year horizon. On June 25, Surf Air Mobility named Wheels Up the launch customer for its Palantir-powered BrokerOS product. On June 29 came two more: the NVIDIA deployment engine and an expanded Surf Air partnership. By July 1, Palantir was leading a broad AI-software rally while much of the AI-infrastructure complex sold off.

No single item explains a $21.7 billion move. The cluster does: three different constituencies — the Pentagon, a large ad-tech platform, and the most important company in AI hardware — independently chose Palantir as plumbing in the same nine days.

The NVIDIA pact is distribution, not dollars

Start with what was actually announced. Palantir’s June 29 release describes an engine for deploying NVIDIA Nemotron open models in sovereign environments — U.S. government agencies and critical-infrastructure operators that need frontier-model capability without letting data, models or intellectual property leave their control. NVIDIA brings the compute stack and open models; Palantir brings AIP, Foundry, its Ontology layer and Apollo, the deployment system that already runs software in classified and air-gapped settings.

It extends the Sovereign AI Operating System Reference Architecture the two companies published in March — a full-stack AI data center design, built around NVIDIA’s Blackwell Ultra systems and CUDA-X libraries, for facilities where data never leaves the building.

Notice what is missing from both announcements: a number. No contract value, no revenue commitment, no backlog entry. That is not a weakness of the story; it is the story. NVIDIA sells the racks and needs someone to make them useful inside SCIFs, utilities and defense ministries — places AWS, Azure and Google Cloud structurally cannot serve. Palantir needs its platforms to be the assumed choice when that spending arrives. A reference architecture with NVIDIA’s logo on it makes Palantir something close to the default operating layer for sovereign AI, the way selling through hyperscaler marketplaces once made cloud software default choices.

The timing sharpened the effect. The same morning, Meta’s reported plan to sell its surplus AI compute was hammering the companies that rent GPUs for a living. Owning the trust layer — the part of the stack that decides whether AI can run in a secure environment at all — suddenly looked like the more defensible business.

NGC2 is the quieter win, and the more bankable one

The Army announcement drew fewer headlines than NVIDIA and deserves more attention. After operational validations with the 4th and 25th Infantry Divisions, the Army fixed its NGC2 common data layer baseline: Foundry as the cloud data layer, Anduril leading the baseline with its Lattice edge mesh, and Raft supplying the data registries. A division-scale, force-on-force validation at the National Training Center — Project Convergence Capstone 6 — follows in July.

Again, no new contract dollars were disclosed, and the honest reading keeps Anduril’s leading role in frame. But data-layer positions in generational programs compound in a way press-release partnerships do not. Once an army standardizes its data ontology on a platform, every subsequent application, contractor and upgrade cycle inherits that choice. Palantir’s U.S. government revenue grew 84% year over year in the first quarter, to $687 million — a run that already includes wins like the $300 million USDA modernization contract. NGC2 moving from prototype toward production is how that line keeps compounding into the 2030s.

The small print: getting paid in a customer’s stock

Then there is the part of the week that deserves a skeptical eye, because the dollar amounts are small and the structure is unusual.

The Wheels Up deal, per Surf Air’s 8-K, is an $8.0 million two-year subscription with a $4.2 million extension option — real money for Surf Air, but revenue that flows to Surf Air, not Palantir, even though Palantir’s Foundry and AIP power the product. Palantir’s own compensation runs through a stranger channel: a prospectus supplement registered 4,761,905 Surf Air shares issued to Palantir “as consideration for license fees and related professional services” — payment in stock, worth about $5 million at the June 23 price. A Schedule 13G filed July 1 shows Palantir now owns 8,248,989 shares, roughly 7.4% of the company.

Set against $1.6 billion in quarterly revenue, an $8.7 million equity stake is a rounding error. The reason to watch it is the pattern, not the size. Palantir booking license revenue paid in a micro-cap customer’s shares is exactly the kind of arrangement TECHi’s audit of Palantir’s AI revenue quality argued investors should separate from organic, cash-paying demand. There is also a genuinely constructive reading: Surf Air is doing the hard work of turning Foundry into vertical aviation software and selling it with its own salesforce, and Wheels Up signing as an enterprise customer is evidence the model works. Both readings can be true. The discipline is refusing to let a $5 million stock-for-services deal carry billions of dollars of narrative weight.

Zeta Global sits between the poles. Rebuilding an ad-tech data cloud on Foundry is real commercial pull into a new vertical — but the widely quoted number attached to it is Zeta’s own multi-year projection, not a contracted figure.

The stock fell 41% while the business accelerated

None of this week’s news would have moved the stock 7.8% if 2026 had not already beaten it down.

Palantir closed at $181.68 on January 7 — its 2026 peak, worth about 57 times the revenue guidance it would later issue for the year. By June 25 it closed at $107.27, a 41% drawdown, compressing that multiple to roughly 34 times. The de-rating happened while the numbers went one direction: up. The first-quarter report posted revenue of $1.633 billion, up 85% year over year — the company’s fastest growth ever — with U.S. commercial revenue up 133%, U.S. commercial remaining deal value up 112% to $4.92 billion, a 46% GAAP operating margin, GAAP net income of $871 million and $8.0 billion in cash. Alex Karp’s letter bragged about a Rule of 40 score of 145%. Guidance for the full year rose to $7.65–7.66 billion, 71% growth. The market’s response, as TECHi noted at the time in its coverage of the range-bound reaction to a blowout quarter, was to keep selling: the stock fell the session after the print and kept grinding lower into late June.

That is a valuation regime change, not an execution problem. At 50-plus times forward revenue, even 85% growth needs years of flawless compounding to justify the price, and the market’s patience with AI multiples shortened twice this year — once in February, again in June. What July 1 did was reattach part of the narrative premium at a lower base: at $125.73, Palantir trades near 39 times this year’s guided revenue, cheaper than January by a third with objectively better fundamentals and two new strategic anchors. Live pricing and the full financial picture are on TECHi’s Palantir quote page.

What $21.7 billion actually bought

Add up every dollar figure disclosed across the week — the $12.2 million Wheels Up subscription that belongs to Surf Air, the $8.7 million equity stake, Zeta’s aspirational $100 million a year — and the news behind Palantir’s $21.7 billion single-day repricing totals well under 1% of it. The other 99% is the market paying for three positions: default deployment vendor for sovereign AI alongside NVIDIA, the data layer under the Army’s most important program, and proof that partners will now build and sell products on Palantir’s platforms with their own capital.

Positions like those are either worth enormous amounts or very little, and the deciding variable is conversion: whether architecture documents and baselines become named, dollar-denominated contracts before the multiple’s patience runs out again.

What to watch from here

Project Convergence Capstone 6 runs at the National Training Center in July — a division-scale NGC2 validation whose outcome shapes when prototype money becomes production money. Palantir’s second-quarter report lands in early August against guidance of $1.797–1.801 billion; the tell will be U.S. commercial remaining deal value and whether any sovereign-AI deployments under the NVIDIA architecture show up as named contracts. Internationally, a single government signing for an AIOS-style deployment would convert the reference architecture from marketing into backlog. And the Surf Air structure is worth tracking each quarter — not because $8.7 million matters, but because a second and third partner paid in equity would make it a strategy, and strategies deserve their own line in the model.

The 2026 de-rating cut the price of Palantir’s machine by a third while the machine sped up. July 1’s buyers are betting that machine plus the new positioning is worth more than 39 times revenue. The next earnings print, not the next press release, settles it.

Not investment advice. This article is for information only. High-multiple AI stocks are volatile, and partnership announcements without disclosed contract values describe positioning, not revenue. Figures reflect trading on July 1, 2026 and filings available at publication. Do your own research before making investment decisions.