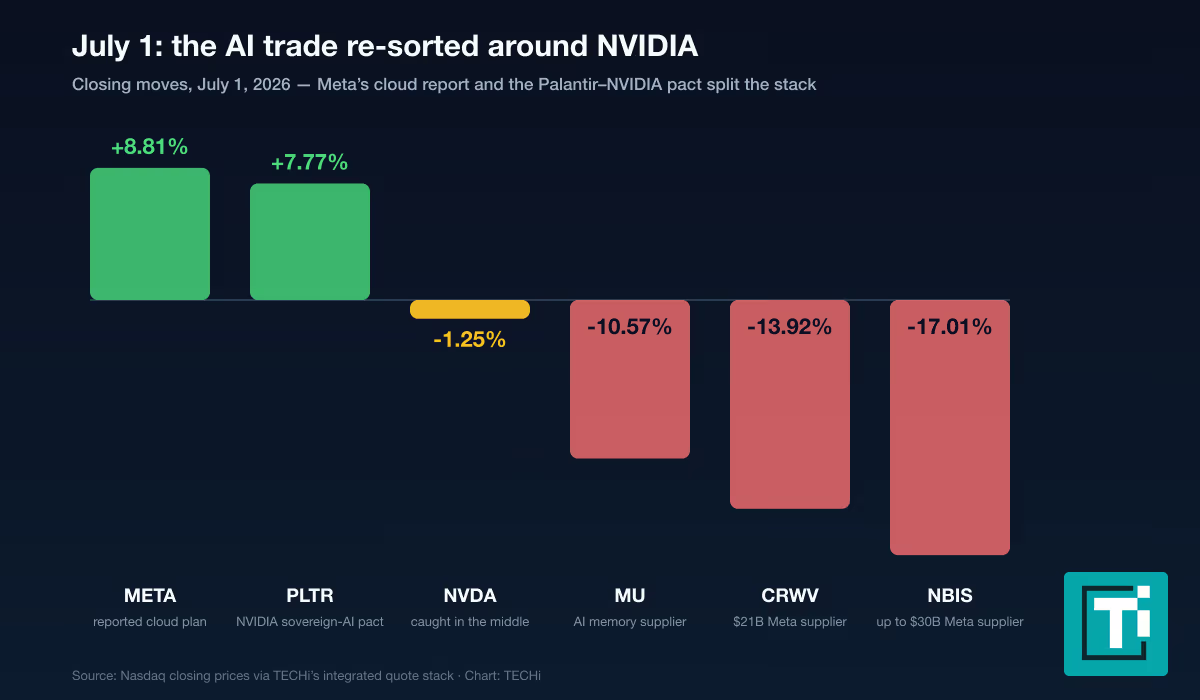

NVIDIA closed at $197.58 on Wednesday, July 1, 2026, down 1.25%. In a normal tape that is rounding error. On this tape it was the strangest print of the day — because everything around NVIDIA moved violently, in both directions, for reasons that all run through NVIDIA’s chips.

A Bloomberg report that Meta plans to sell its surplus AI computing power tore 10% to 17% off the companies that buy NVIDIA GPUs to rent them out. A sovereign-AI partnership built on NVIDIA’s own platform sent Palantir up 7.8%. Meta, the customer at the center of both stories, gained 8.8%. The company whose silicon sits under every one of those trades slipped a quiet 1.25% — which, at NVIDIA’s size, still meant roughly $61 billion of market value gone, more than the day’s headline casualty, Nebius, lost in total.

That flat close is worth more attention than it got. July 1 handed NVIDIA both halves of the only question that matters at a $4.8 trillion valuation — who buys the next half-trillion dollars of GPUs — in a single session. One signal said the current buyers may be full. The other showed the next buyer class being assembled in public. The market shrugged because the two roughly cancel. They will not cancel forever.

Article Brief

Key Takeaways

5 Points30s Read

- The quiet numberNVDA slipped 1.25% to $197.58 on July 1 — a ‘small’ move that erased roughly $61 billion, more than Nebius, the day’s headline casualty, lost in total.

- Signal oneMeta’s reported plan to resell surplus AI compute is the first credible sign NVIDIA’s largest buyer class ordered ahead of need — a secondary market for GPU-hours competes with new chip sales.

- Signal twoThe Palantir sovereign-AI engine, built on NVIDIA Blackwell Ultra reference designs, opens governments and critical infrastructure as the next buyer class — and NVIDIA re-segmented its reporting in May to make that shift visible.

- The footnote that mattersNVIDIA’s stakes in private AI companies hit $42.3 billion in April — up from $3.4 billion a year earlier — blurring the line between organic and vendor-financed demand.

- The tell aheadThe late-August report is the first under the new Hyperscale vs. ACIE split. The ACIE line shows whether the next buyers are arriving fast enough to replace any hyperscale slowdown.

The $61 billion dip that didn’t make headlines

Set the day’s moves side by side and the asymmetry is the story. Nebius fell 17% and erased about $11.9 billion — front-page material, covered in TECHi’s report on the Meta backstop that repriced. CoreWeave dropped 13.9%, Micron 10.6%. NVIDIA’s 1.25%, applied to 24.2 billion shares, removed roughly five Nebius-sized losses without producing a single headline about NVIDIA.

The quiet extends further back. NVIDIA closed 16% below its May 14 record of $235.74 — a de-rating that began weeks before Meta’s cloud plans leaked — while remaining up about 4.6% for 2026. The market has been slowly repricing the world’s most valuable company all quarter. July 1 just made the reasons legible.

Signal one: the biggest buyers say they have spare

The Bloomberg report says Meta is planning a cloud business that would sell access to its AI computing power and models. Most coverage treated that as a story about Meta versus the neoclouds. It is more uncomfortable than that for the chip supplier, because of what reselling implies about the buying.

Meta has spent a year hoovering up external compute: an agreement with CoreWeave expanded to $21 billion in April, Nebius contracts worth up to $30 billion including the March agreement’s $27 billion, a $10 billion Google Cloud deal — more than $60 billion of disclosed third-party commitments, stacked on top of its own data center construction. A company that assembled that position and now says it expects surplus is telling the market something about the gap between what it ordered and what it needs.

The mechanism that should worry NVIDIA holders is the secondary market. Every GPU-hour Meta resells is compute that some developer does not buy as a new chip, from NVIDIA, through some other channel. Used-capacity markets are how every hardware cycle ends its scarcity phase: the product stops being rationed and starts being brokered. If more hyperscalers follow — and reselling surplus is contagious, because nobody wants to be the one holding idle capacity — order books stop being a clean read on demand, and the double-ordering that fed the boom starts unwinding.

The honest counterweight: a Meta cloud business is also, mechanically, a new hyperscaler. Serving outside customers at scale would require Meta to keep buying NVIDIA silicon, possibly faster than its own models alone would justify. Resale can mean saturation, or it can mean a fourth cloud giant being born inside NVIDIA’s best customer. The report alone cannot distinguish the two — which is the real reason NVDA fell 1% rather than 10%.

Signal two: NVIDIA is manufacturing its next buyer class

The same session delivered the other half of the answer. Palantir’s 7.8% surge — dissected in TECHi’s coverage of what the NVIDIA deal really buys — came from a June 29 launch of an engine for deploying NVIDIA’s Nemotron open models in sovereign environments, built on the Sovereign AI Operating System Reference Architecture the two companies published in March: a full-stack AI data center design around Blackwell Ultra systems for facilities where data never leaves the building.

Governments, defense ministries, utilities and hospitals cannot put their workloads on AWS, and they are precisely the buyers a reference architecture with NVIDIA’s name on it is built to unlock. This is NVIDIA doing deliberately what it did accidentally with the hyperscalers: creating a class of customers whose capex plans assume NVIDIA as the default.

The tell that this is strategy rather than press-release garnish sits in NVIDIA’s own reporting. In its May 20 results, NVIDIA announced it is re-segmenting Data Center into two sub-markets: Hyperscale, for the public clouds and consumer internet giants, and ACIE — AI Clouds, Industrial and Enterprise — for everything else, including the sovereign AI factories. Companies redesign their segments when they want investors watching a mix shift. One month before Meta signaled that hyperscale buying may have run ahead of need, NVIDIA quietly built the reporting line that will show whether the next buyers are arriving fast enough to matter.

The May 20 report supplied the scale of what needs replacing, or extending: record revenue of $81.6 billion, up 85% year over year, with Data Center at $75.2 billion — compute up 77%, networking up 199% — and a second-quarter guide of $91.0 billion that assumes zero Data Center compute revenue from China. Growth like that is why a 1.25% dip costs $61 billion. It is also why any wobble in the buyer mix moves more money than most companies are worth.

The balance sheet started answering in May

There is a third character in this story, and it lives in a footnote. Note 6 of NVIDIA’s April 10-Q shows non-marketable equity securities — stakes in private companies, overwhelmingly in the AI ecosystem — of $42.3 billion, up from $22.3 billion a quarter earlier and $3.4 billion a year ago. NVIDIA added $17.9 billion of these positions in the April quarter alone and booked $2.6 billion of unrealized gains through other income. Among them: a $2 billion investment in Nebius, which Nebius’s own shareholder letter calls the largest deal in its history — equity in a customer whose job is buying NVIDIA GPUs.

TECHi called this dynamic the bank of the AI buildout in May, when the book was half this size. The 10-Q makes it measurable, and it sharpens the July 1 question. When NVIDIA funds the AI clouds that buy its chips, reported demand and financed demand blur — and a Meta-style surplus signal is exactly the event that tests how much of the order book is organic. It cuts the other way too: GAAP net income of $58.3 billion exceeded operating income of $53.5 billion last quarter, meaning investment gains are now a meaningful earnings line that rides the same cycle the chips ride. In a downturn, the same book amplifies in reverse.

The capital-return pivot completes the picture. NVIDIA returned a record $20 billion to shareholders in the quarter, added an $80 billion buyback authorization, and raised its dividend from $0.01 to $0.25 — a 25-fold increase. A company generating cash faster than even an $18-billion-a-quarter ecosystem investment program can absorb is a wonderful problem, but it is a mature company’s problem, arriving while the stock still carries hypergrowth expectations at roughly 13 times the revenue run-rate implied by its own guide.

The third demand signal is priced at zero

There is a third buyer class in this story, and NVIDIA currently values it at nothing: China. The $91 billion outlook, in the company’s own words from the May release, “is not assuming any Data Center compute revenue from China.” A market that once absorbed a double-digit share of NVIDIA’s data center output is carried in the guide as a hard zero, after years of export-rule whiplash that TECHi has tracked since the H200 era.

That zero does two things to the July 1 math. It means the 85% growth rate is being produced entirely by the buyers whose appetite Meta’s report just put in question — which sharpens the concentration concern rather than softening it. And it means any durable reopening of Chinese data-center demand, whether through license changes or compliant product lines, lands as pure upside on a guide that already clears $91 billion without it. Optionality that large rarely trades at exactly zero, but that is where NVIDIA’s own outlook puts it.

It also functions as a quiet hedge against the surplus problem. If hyperscale ordering decelerates while resale spreads, license relief in even a single quarter would cover a great deal of Meta-sized wobble. Watching Washington is now part of reading the order book — a strange sentence that happens to be true of the world’s most valuable company.

What a flat close is actually pricing

NVIDIA enters the second half of 2026 sixteen percent below its record with the strongest income statement in corporate history and two open questions the July 1 tape put on the same page. If Meta-style resale spreads before sovereign and enterprise demand scales, hyperscale orders decelerate into an air pocket — the timing gap is the bear case, not the end state. If the ACIE buyers arrive on schedule — Vera Rubin systems begin reaching customers in the second half of 2026, per deployment schedules already public in supplier filings — the buyer handoff happens without the air pocket, and the current multiple looks conservative. Live pricing sits on TECHi’s NVIDIA quote page.

A market that believed the first story would not leave NVDA within 5% of $200. A market that believed the second would not have let it fall 16% from May. The flat close is not indifference; it is an unresolved argument, held at roughly 13 times forward revenue.

What to watch from here

The next quarterly report, expected in late August against the $91 billion guide, will be the first under the Hyperscale-versus-ACIE split — making the ACIE line the single most informative new number in AI investing: it is where sovereign deals, national AI factories and enterprise buildouts either show up or don’t. Meta’s late-July earnings call comes first, and any commentary that moves its cloud plan from report to product changes the resale math for every supplier. Watch, too, whether the NVIDIA–Palantir architecture lands a named government deployment — the conversion event that turns reference designs into backlog — and the next 10-Q’s Note 6: if ecosystem investments keep running at $15–18 billion a quarter while customers talk about surplus, the line between demand and vendor financing deserves the skepticism it drew in older cycles.

July 1 compressed NVIDIA’s decade into one session: the old buyers signaled fullness, the new buyers signaled arrival, and the stock split the difference. The ACIE line in August starts settling which signal was the loud one.

Not investment advice. This article is for information only. Mega-cap AI stocks move on reports and partnerships whose financial terms are often undisclosed; figures here reflect trading on July 1, 2026 and SEC filings available at publication. Do your own research before making investment decisions.