Two things about the price of artificial intelligence became true on Wednesday, July 1, 2026, and they point in opposite directions. At midnight, a roughly 20% increase in what AWS charges for reserved NVIDIA GPU capacity took effect — announced quietly the week before. By mid-morning, Bloomberg was reporting that Meta plans to sell its surplus AI compute to outsiders. The world’s biggest cloud raised the rent on scarce silicon the same day the market learned a $1.7 trillion neighbor thinks the stuff is abundant enough to resell.

Amazon shares closed at $241.70, up 1.4% — about $36 billion of added market value on a day the GPU-rental complex lost multiples of that. The quiet gain was a verdict: the market looked at scarcity pricing and secondary supply arriving in the same session and decided that, for now, Amazon sits on the right side of both.

That verdict deserves more scrutiny than it got, because the two signals cannot both stay true forever. One of them describes the present. The other describes 2027. And Amazon’s stock, more than any other in the AI trade, is a bet on how gracefully the first hands off to the second.

Article Brief

Key Takeaways

5 Points30s Read

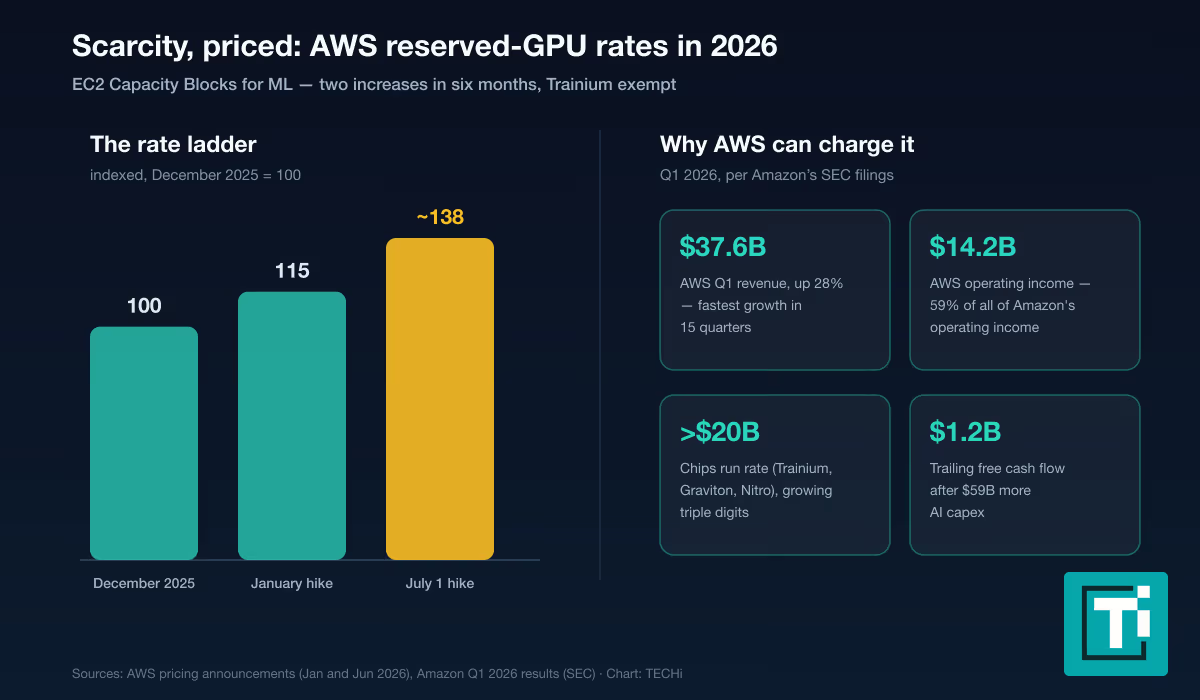

- The hikeAWS raised reserved NVIDIA GPU rates about 20% effective July 1 — its second increase in six months, compounding to roughly 38% since December. Trainium, its own chip, was exempt both times.

- The collisionThe increase took effect the same day Bloomberg reported Meta plans to sell surplus AI compute. Scarcity pricing and secondary supply hit the tape together; AMZN rose 1.4%, adding about $36 billion.

- The engineAWS grew 28% in Q1 — fastest in 15 quarters — and produced $14.2 billion of operating income at a 37.8% margin: 59% of all of Amazon’s operating profit from about a fifth of its revenue.

- The reason for the hikeTrailing free cash flow collapsed to $1.2 billion as AI capex rose $59.3 billion. Scarcity pricing is how the buildout pays for itself before depreciation lands.

- The real Meta riskNot stolen customers — broken pricing. A secondary market for GPU-hours in 2027 would hit AWS margins exactly when this year’s capex depreciates through the income statement.

The price increase that broke a 20-year habit

Start with what AWS actually did. On June 26 it notified customers that EC2 Capacity Blocks for ML — scheduled reservations of NVIDIA GPU capacity — would cost about 20% more from July 1. Under the new schedule, a P6-B300 accelerator runs $14.04 per hour; P5 capacity runs $5.19 in U.S. regions. Other purchasing options were left unchanged, and Trainium — Amazon’s own AI silicon — was pointedly exempt.

This was not a one-off. AWS raised the same rates about 15% in January, which makes the compounded increase since December roughly 38%. Renting a reserved NVIDIA GPU on AWS now costs about a third more than it did six months ago.

For this company, that is close to a change of identity. AWS built its brand on the opposite motion — years of price cuts, marketed as the natural dividend of scale. Raising prices twice in six months on its hottest product says something simple and loud: at the margin, demand for dedicated AI compute still exceeds supply, and AWS has decided to ration by price rather than by queue. Companies do not volunteer for headlines about making AI more expensive unless the order book lets them.

The Trainium exemption is the strategy inside the strategy. Every increase on NVIDIA-based capacity widens the price gap in favor of Amazon’s own chips — a nudge repeated at billing scale. Make the scarce thing expensive, keep the substitute you own cheap, and let ten thousand CFOs do the steering for you.

What a reservation actually costs now

Abstract percentages hide how much money moves when a rate card changes, so translate the new schedule into a real bill. A modest training cluster — eight P6-B300 nodes, sixty-four accelerators — reserved around the clock for thirty days now costs about $647,000 at the new $14.04 hourly rate. Before July 1 the same block ran roughly $539,000; before January, closer to $469,000. One mid-sized reservation, one month, is $178,000 more expensive than it was in December — and frontier labs reserve capacity in multiples of that, for quarters at a time.

Scale that across AWS’s reservation book and the hikes read as a material revenue lever that required no new hardware, no new regions and no announcement beyond a pricing-page update. It also explains the calm in the stock: price increases on committed, scheduled capacity convert directly into the segment margin investors watch most, with the cost base already built.

The other signal, six hours into the trading day

Then came the Bloomberg report: Meta is planning a cloud business to sell access to its AI computing power and models. The companies that rent GPUs for a living took the hit — Nebius fell 17% and CoreWeave almost 14%, a repricing TECHi dissected in its report on the Meta backstop that changed meaning — because their anchor tenant had just described itself as oversupplied.

Set the two signals side by side and the apparent contradiction resolves into a timeline. AWS’s price increase describes the present: reservations for current-generation NVIDIA silicon, deliverable now, in a market where every hyperscaler and neocloud is still capacity-constrained. Meta’s surplus describes the future: the capacity it has contracted comes online in tranches through 2027, and reselling it is a plan, not a product. AWS priced today’s scarcity. Meta signaled tomorrow’s abundance. The uncomfortable question for Amazon shareholders is not which signal is right — both probably are — but what happens to a freshly price-hiked P&L when the second one arrives.

The quarter that explains the confidence

AWS is negotiating from the strongest position it has held in years, and the numbers are unambiguous. Amazon’s first-quarter results, filed April 29, showed AWS revenue of $37.6 billion, up 28% year over year — in Andy Jassy’s words, “our fastest growth in 15 quarters” on a very large base. AWS operating income reached $14.2 billion at a 37.8% margin. That single segment, roughly a fifth of Amazon’s revenue, produced 59% of its operating income.

The same release carried the numbers that make the Meta threat less existential than it sounds. Amazon’s chips business — Trainium, Graviton and Nitro — passed a $20 billion annual revenue run rate, growing triple-digit percentages. OpenAI committed to consume approximately two gigawatts of Trainium capacity through AWS infrastructure. Advertising passed $70 billion in trailing revenue. Total net sales rose 17% to $181.5 billion, and net income doubled to $30.3 billion — a figure flattered by $16.8 billion in pre-tax gains on Amazon’s Anthropic investments, the same ecosystem-stake pattern that has quietly become a feature of every AI giant’s income statement.

A cloud growing 28% with an in-house silicon franchise tripling and a two-gigawatt anchor tenant on that silicon is not a business trembling before a rival that has not yet named a product. It is, however, a business whose economics depend on one assumption holding — which brings up the strangest number Amazon reported this year.

The $16.8 billion asterisk

One line in the first-quarter release deserves separate handling before it flatters anyone’s model. Net income of $30.3 billion — nearly double a year earlier — includes $16.8 billion of pre-tax, non-operating gains from Amazon’s investments in Anthropic. That is a mark on a private stake, not cash from selling servers or shipping parcels, and marks can reverse.

The pattern is now industry-standard: every AI giant carries a book of stakes in its own ecosystem, and those stakes swing reported earnings in the same direction as the cycle that drives the underlying business. The discipline for anyone valuing Amazon stock is to price the operating engine — $23.9 billion of operating income, growing on AWS and advertising — and treat the investment gains as a cyclical amplifier rather than a run rate. In a good year the asterisk adds billions; in a repricing year, the same line subtracts them.

The $1.2 billion number that explains the hike

For the twelve months ended March 31, Amazon generated $148.5 billion of operating cash flow, up 30% — and $1.2 billion of free cash flow, down from $25.9 billion a year earlier. The gap is capital expenditure: purchases of property and equipment rose $59.3 billion year over year, an increase the filing attributes primarily to investments in artificial intelligence.

Read the price hike against that line and it stops looking opportunistic. Amazon is spending at a pace that consumes essentially all of its prodigious cash generation; the roughly 38% compounded increase in reserved-GPU rates is how that spending starts paying for itself before the depreciation bill lands. Scarcity pricing is the bridge between the capex and the return — the mechanism TECHi’s earlier analysis of Amazon’s margin ladder argued would decide the stock, and the reason its companion piece asked whether logistics could pay for the AI buildout if cloud margins wobbled.

That is the precise shape of the Meta risk. It is not that enterprises will move their workloads to a social-media company’s cloud next quarter; they will not. It is that a secondary market for GPU capacity — Meta reselling surplus at marginal cost, and other over-provisioned buyers following — breaks the scarcity pricing AWS just exercised, in 2027, exactly when Amazon’s depreciation from this year’s $59 billion capex step-up is flowing through the income statement. The hike and the threat are aimed at the same line item, from opposite directions, two years apart.

Amazon is already the company Meta wants to become

There is an irony in the July 1 pairing worth naming. Meta’s reported plan — monetize spare compute, sell hosted model access — is a description of how AWS itself was mythologized at birth: excess capacity, turned outward, becoming a business. Twenty years later that business produces the majority of Amazon’s profit. Meta is not attacking AWS so much as trying to replicate its founding trick, two decades late, without the enterprise relationships, the compliance certifications, the 200-service catalog or an anchor customer like OpenAI committing gigawatts to its silicon.

If Meta’s cloud undercuts anyone on price, it undercuts the commodity layer — raw GPU-hours — which is precisely the layer Amazon is de-emphasizing as it steers customers toward Trainium and up the stack toward Bedrock and managed services, where the pricing power demonstrated on July 1 actually lives. The neoclouds sell the commodity; that is why they fell double digits. Amazon sells the commodity, the substitute and the layer above it — which is why it rose. The competitive lesson of the day was less about Meta versus Amazon than about where in the stack a moat survives a supply glut: one layer up from wherever the glut happens.

The stock has already voted once this year

Amazon’s 2026 chart is the whole argument in miniature. The stock fell from $247 in early January to $198.79 by February 13 — the AI-capex scare, when that vanishing free cash flow first spooked the market. Then the April 29 report reframed the spending as fuel for a 28%-growth AWS, and the stock ran to a record $274.99 by May 6. It enters July at $241.70 — up 6.7% for the year, 12% below the record, valued near $2.6 trillion on 10.76 billion shares. Twice this year the market has changed its mind about whether $59 billion of incremental AI capex is a problem or a weapon; the July 1 session was a small third vote for weapon. Live pricing sits on TECHi’s Amazon quote page.

What settles it on July 30

Amazon reports second-quarter results on July 30, and the print now carries an unusual question: the first evidence of what a price-hiked AWS looks like. The January increase was live for the full quarter — AWS revenue growth holding near 28% would confirm the hikes are landing on demand inelastic enough to pay them. Watch the margin line for the same reason: 37.8% with rates up again on July 1 implies the third quarter could print AWS margins the segment has never shown. Beyond the cloud numbers: the chips run rate against the $20 billion mark, any update on the OpenAI Trainium ramp, capex guidance for the back half, and the Anthropic carrying value that swung net income by $16.8 billion last quarter. And in the background, the only Meta question that matters for this stock — whether the reported cloud plan becomes a priced product — because the day surplus GPU-hours get a public rate card is the day AWS’s scarcity pricing meets its first real test.

Not investment advice. This article is for information only. Cloud pricing schedules change, reported plans may never become products, and quarterly results can differ materially from expectations. Figures reflect trading on July 1, 2026 and filings and announcements available at publication. Do your own research before making investment decisions.