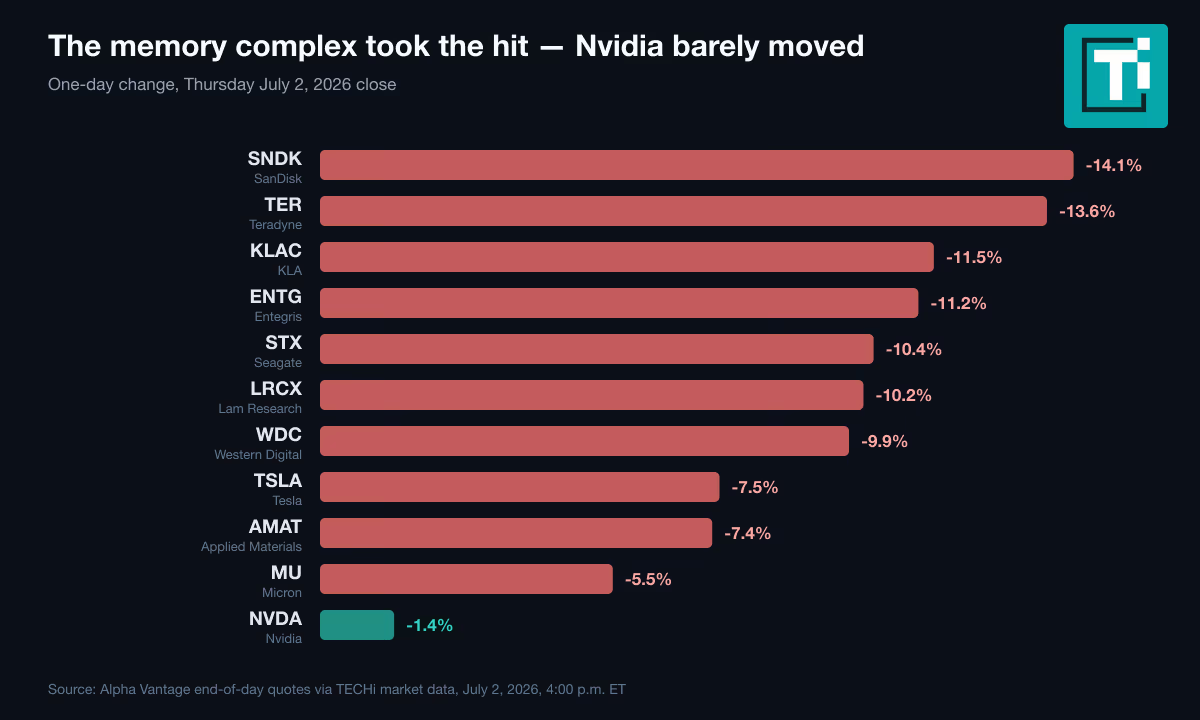

Thursday’s selloff priced in an AI memory glut that, on every published construction timeline, does not exist yet. SanDisk closed down 14.1% at $1,745. Teradyne lost 13.6%, KLA 11.5%, Seagate 10.4%, Lam Research 10.2%. The Philadelphia Semiconductor Index fell 5.4% on top of Wednesday’s 6.3% — an 11.4% wipeout in two sessions — while the Dow rose 595 points to a record close of 52,900.07. Thursday was not a market panic. It was a targeted unwind of the single most profitable trade of 2026.

It may also already be aging badly. Hours after Wall Street shut down for the long July 4th weekend, Seoul — the market that started the rout — took most of it back. The KOSPI jumped 5.76% to 8,088.34 on Friday, Samsung Electronics rose 8.7%, SK hynix gained more than 10%, and the Korea Exchange triggered a buy-side sidecar to slow the rally rather than the crash. US markets stay closed until Monday, July 6. That leaves three days between the fear and the next print — enough time to check whether the glut thesis survives its own arithmetic.

Market Brief

Key Takeaways

5 Points30s Read

- No downgrade started thisThe selloff chained three headlines — Korea’s ₩800 trillion fab plan, Michael Burry’s chip shorts, and Meta’s reported compute-leasing business — into a glut narrative inside 72 hours.

- The supply arrives in the 2030sThe four new Korean fabs produce nothing before 2033 at the earliest; the five-year DRAM-doubling goal leans on accelerating fabs already under way.

- Prices are still rising nowTrendForce’s actuals show conventional DRAM contract prices up 93–98% in Q1 2026 and another 58–63% in Q2, with Q3 rising more slowly — decelerating, not falling.

- Thursday’s tape contradicts itselfEquipment makers fell hardest, yet they are the direct beneficiaries of the capex the market says it fears. Nvidia slipped just 1.4% while the Dow closed at a record.

- Seoul already reconsideredThe KOSPI rebounded 5.76% on Friday with SK hynix up about 11% — while US markets stay closed until Monday, July 6.

Three headlines walked into a crowded trade

There was no downgrade behind Thursday’s damage, and no earnings miss. The selloff assembled itself out of three separate headlines that hit an extremely crowded trade inside 72 hours.

The first came Monday, June 29, when President Lee Jae Myung’s government unveiled a program under which Samsung and SK hynix will each build two new memory fabs in Korea’s southwest — 800 trillion won of investment, roughly $518 billion, with a stated goal of doubling the country’s DRAM capacity within five years. Worth remembering: Korean equities did not treat that announcement as bearish. The KOSPI barely moved on it.

The second landed Tuesday, June 30, when Michael Burry disclosed short positions — as reported by Yahoo Finance and others summarizing his paywalled Substack — in Nvidia at $198.09 and Applied Materials at $729.40, a Tesla short at $416.22, a first-ever Caterpillar short at $1,060.98, and SOXX puts rolled out to March 2027. He called the semiconductor index “a pure form of overvaluation,” noted it was trading roughly 65% above its 200-day moving average — a gap seen only once before, in 2000 — and framed the Korean plan bluntly: “I see this as the beginning of the end. It’s now just a matter of time.”

The third was the strangest. On Wednesday, July 1, Bloomberg reported that Meta is building “Meta Compute,” a cloud business that would sell excess AI computing power and hosted models. Meta shareholders loved it — the stock closed up 8.8% at $612.91. Memory investors heard something else: the word “excess” attached to AI infrastructure for the first time. Korea traded on it first, and Thursday morning in Seoul the KOSPI fell 7.89% in what Seoul Economic Daily dubbed the “Meta Shock” — SK hynix down 14.57%, Samsung down 9.06%, a sell-side sidecar freezing program trades minutes into the session, and roughly ₩4.4 trillion of foreign selling. When New York opened, the same logic ran through every US name that touches memory, storage, or the machines that make them.

The dispersion inside Thursday’s tape is the first clue that this was a thesis trade, not a demand scare. Nvidia — the company actually buying the memory — slipped 1.4%. Axcelis lost 19%, Ultra Clean 17.8%, FormFactor 16%. The Dow set a record the same afternoon, lifted by a June payrolls print of 57,000 that came in well under the roughly 110,000 economists expected and firmed up rate-cut bets. Nobody sold AI on Thursday. They sold the suppliers of AI’s most crowded input.

The bear case deserves better than a strawman

Memory is the most violently cyclical corner of the chip industry, and the people selling it on Thursday know the history. Every memory upcycle for three decades has ended the same way: prices go vertical, supply gets announced, supply arrives, prices collapse. In 2018 the DRAM makers expanded into a hyperscaler spending pause and Micron lost roughly half its value in months. The glut camp is not inventing a risk. It is pattern-matching to the only pattern this industry has ever produced — and now the supply response has a press conference and a number attached: ₩800 trillion.

There is even a courtroom version of the tightness argument. A class action filed June 25 in the Northern District of California — Garciaguirre v. Samsung Electronics — accuses Samsung, SK hynix and Micron of curtailing DDR3 and DDR4 output in concert, using the shift to HBM as cover, and inflating conventional DRAM prices by roughly 700% over four years. Those are allegations, nothing more; a similar suit in 2018 was dismissed, though Samsung and Hynix did plead guilty to DRAM price-fixing in 2005. But seventeen plaintiffs just attached a number to how abnormal this pricing cycle feels to the people paying for it.

Valuation adds the third leg. Morningstar’s Lorraine Tan told Bloomberg TV that AI-linked names are “priced for perfection” and that she expects a “20, 30% correction for a good percentage of the names we cover” before they become worth buying again — her argument being that the market is extrapolating today’s growth clear through 2028.

And capex itself is the cycle’s fuel gauge. Microsoft guided 2026 capital spending to about $190 billion, roughly 23% above what analysts had modeled; Meta raised its own 2026 range to $125–145 billion in April, citing component costs. Budgets do not compound at 60% forever. When they flatten, memory pricing is the first casualty. If 2026 turns out to be peak AI capex, Thursday’s sellers will have been early rather than wrong.

The math the selloff skipped

Take the glut case apart piece by piece, though, and one thing is missing from every component: a date.

Start with the supply itself. The four new Korean fabs produce nothing this decade. SK hynix’s fourth Yongin fab was pulled forward to 2033 — from 2045 — and the Honam megafabs are mid-2030s projects; as TweakTown noted, most of the new capacity “will not arrive until well into the next decade.” The five-year capacity-doubling goal rides on accelerating fabs already underway, like Samsung’s P5 and P6 at Pyeongtaek — and fab megaprojects have a long industry record of slipping, not accelerating.

Now the prices that supply is meant to crush. TrendForce forecast record first-quarter contract-price increases across every memory category in February — conventional DRAM up 90–95% quarter over quarter, PC DRAM more than doubling. The actuals came in at 93–98%, with DRAM industry revenue up 81% in a single quarter. Second-quarter contracts added another 58–63% for DRAM and 70–75% for NAND. The third-quarter forecast still points up, just more slowly. That deceleration is the closest thing to a glut signal anywhere in the data — and prices rising more slowly are still rising. The squeeze has already reached consumer hardware, pushing up phone and PC memory prices since the spring.

There is also a structural reason the shortage outruns simple capacity math: HBM, the memory AI accelerators need, consumes roughly three times the wafer supply of DDR5 for the same bits, by Micron CEO Sanjay Mehrotra’s own account. Every point of AI demand growth quietly deepens the conventional-DRAM deficit that the lawsuit above describes.

Then there is Micron’s quarter — the freshest fundamental datapoint the industry has, reported June 24 into exactly the test Wall Street had doubled its targets ahead of. Revenue of $41.46 billion, up 346% year over year. Gross margin of 84.9%. Guidance for a $50 billion quarter at 86% margins. HBM booked solid through calendar 2027, per the earnings call. At Thursday’s close of $975.56, Micron trades near eight times the annualized midpoint of its own next-quarter EPS guidance. Whatever an AI bubble multiple looks like, that is not it.

The capex numbers cut the same way. Micron is spending about $27 billion this fiscal year and signaled north of $40 billion next year — spending its enemies call the glut and its suppliers call revenue. Microsoft told investors that $25 billion of its roughly $190 billion capex figure is component-price inflation, mostly memory, with CFO Amy Hood expecting the company to “remain constrained at least through 2026.” Nobody pays a $25 billion inflation surcharge on a component that is about to be oversupplied.

Thursday’s tape argues with itself

Hold the selloff up to its own logic and three contradictions fall out.

The equipment makers fell hardest. Axcelis, Ultra Clean, FormFactor, Teradyne, KLA — down 13% to 19% — are the direct revenue beneficiaries of the ₩800 trillion buildout the market claims to fear; TrendForce flagged the plan as a strain on chipmaking tool supply within a day of the announcement. Selling memory because too much capacity is coming, and simultaneously selling the companies that get paid to build that capacity, coheres only if capex peaks in 2026 and the Korean plan stalls. Those are two different bear cases pulling in opposite directions.

The Meta Compute readthrough inverts under inspection. Excess compute worth building a business around is compute somebody will pay for — TechCrunch’s comparison to SpaceX turning launch capacity into Starlink is the better frame. Scarcity, monetized. CoreWeave and Nebius fell on the report because a competitor showed up, not because demand for compute disappeared.

And Korea itself — the market that lives closest to the memory industry, trades its inventory rhythms daily, and started this rout — reversed most of its own verdict within twenty-four hours. SK hynix up about 11%, Samsung up 8.7%, the KOSPI reclaiming 8,000 while American screens stayed dark. Wall Street has not had the chance to reconsider. Seoul already did.

What the scoreboard says going into Monday

Scale matters here. Even after losing 23.3% in two sessions from its June 30 record close of $2,273.73, SanDisk enters the weekend up 635% for 2026 — it started the year at $237.38. Its first half, at +858%, was the best of any S&P 500 stock, with Micron’s +304% the runner-up. Thursday did not delete the memory trade. It deleted about a fifth of its best year — and forced the question of whether the rest is earned.

The Street’s answer, so far, is yes. Bank of America’s Wamsi Mohan raised his SanDisk target to $2,500 from $2,100 on July 1 — ten times his calendar-2027 earnings estimate of $252 — on the view that NAND stays undersupplied through 2027. Citi’s Asiya Merchant put the same $2,500 on it a week earlier. Against them stand Burry’s puts and Tan’s 20–30% haircut. That is the whole argument in one line: $2,500 or 30% down, from the same starting facts.

The physical layer, meanwhile, has not blinked. SanDisk’s $42 billion contracted backlog already covers more than a third of its fiscal 2027 supply. Western Digital said in February it is “pretty much sold out” of hard drives for calendar 2026. Seagate’s nearline capacity is “almost fully allocated through calendar 2027.” Sold-out order books can absolutely coexist with a falling stock price — that is what a multiple reset is. What they cannot coexist with is a present-tense glut.

Monday, July 6 decides which session was the outlier. Three things are worth watching. Whether US memory names follow Seoul’s Friday or extend their own Thursday. Whether semicap trades with memory or decouples from it — a genuine glut trade keeps them glued together, a sentiment flush lets them separate. And the next round of DRAM contract prints: deceleration keeps the supercycle argument alive, while an outright decline would end it.

The glut is real as a forecast — in memory, supply always comes eventually. Thursday priced “eventually” as “now.” The distance between those two words is where this market trades for the rest of the year.

Investment Disclaimer: This article is for informational and educational purposes only. It is not financial advice and should not be construed as a recommendation to buy, sell, or hold any security. Figures reflect company disclosures, court filings, TECHi market data, and public sources available at the time of drafting. Market data may be delayed, cached, or revised. Always conduct your own due diligence and consult a licensed financial advisor before making investment decisions.