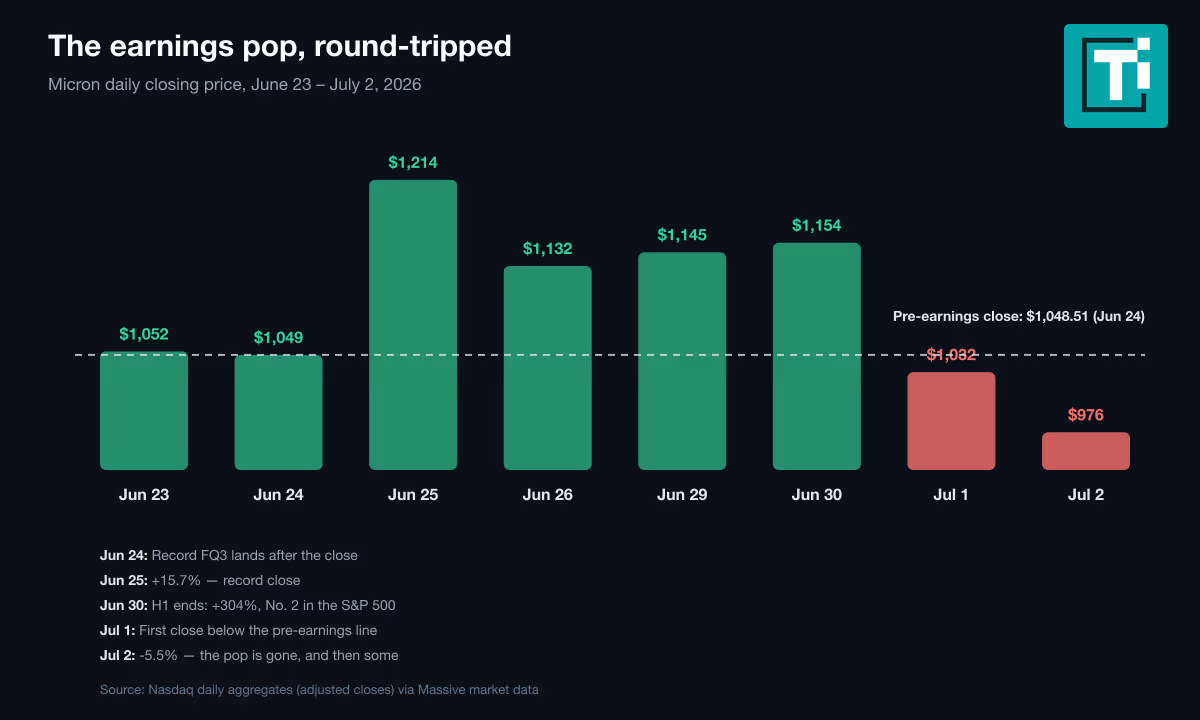

On June 24, one minute after the closing bell, Micron reported the largest quarter any standalone memory company has ever posted: $41.46 billion in revenue, up 346% in a year, at an 84.9% gross margin. The stock jumped 15.7% the next day to a record close of $1,213.56. Five sessions later, all of it was gone — and then some. Micron ended Thursday at $975.56, seven percent below where it traded before the report came out.

That disconnect is the story, and it is worth being precise about what it is not. It is not a miss — the quarter beat everything, and guidance calls for $50 billion next quarter at 86% margins. It is not company news — Micron’s own record since June 24 is nearly silent. A stock that round-trips the best results in its history is the market saying it no longer believes earnings are the question. For memory investors, that behavior has a name, a history, and a famous warning label attached. Whether the label applies this time is the whole debate at $975.

Article Brief

Key Takeaways

5 Points30s Read

- The round trip is completeMicron popped 15.7% on its record June 24 report, then fell 19.6% in five sessions — closing July 2 at $975.56, seven percent below its pre-earnings price.

- The quarter was historic, precisely$41.46B at 84.9% gross margin is a Micron record and the largest quarter any standalone memory company has reported — though Nvidia’s latest ($81.6B) and Samsung’s memory division both dwarf it.

- Cheap is the debate, not the answerAt 6.8x forward earnings, MU echoes its 2018 setup, when a ~4.5x forward multiple at the peak preceded a 57% decline — in memory, trough multiples historically mark cycle tops.

- The company changed nothingMicron filed only routine documents during the slide; the pressure came from glut narratives, a recirculated antitrust suit, and pre-scheduled insider sales near the high.

- Three concrete signpostsSamsung’s preliminary print ~July 7, SK hynix’s late-July report, and Micron’s ~late-September quarter — where the $50B guide either lands or cracks.

The quarter, without adjectives

Superlatives need care here, because the obvious ones are wrong. Micron’s $41.46 billion is not the biggest quarter in chip history — Nvidia reported $81.6 billion for its most recent quarter. It is not even the biggest memory quarter — Samsung’s semiconductor division did about ₩81.7 trillion in the March quarter, with its memory unit alone above Micron’s figure in dollar terms. What it is: a record for Micron by a wide margin, and more revenue than any standalone memory company has ever reported — SK hynix’s all-time record quarter works out to roughly $35.5 billion. It also out-earned scale references that would have sounded absurd two years ago: more quarterly revenue than TSMC’s latest reported quarter, and roughly double Intel’s best quarter ever.

The market’s first read agreed. Shares jumped about 15% the next day, touching an all-time intraday high of $1,255, and seventeen firms raised their targets in a single session. It was exactly the outcome the setup TECHi outlined before the report required: Wall Street had doubled its targets into June 24, and June 24 delivered.

Six sessions, round trip

The sequence looks like a market changing its mind in slow motion, then all at once. June 26: minus 6.7%, the classic sell-the-news fade. June 29 and 30: two quiet green days into the half-year close. July 1: minus 10.6%, the real break — the day Michael Burry’s semiconductor shorts hit the tape and the AI-memory glut narrative took hold. July 2: another 5.5% down as glut fears swept the whole complex, closing the five-session stretch at minus 19.6% — Micron’s worst run since late March, by exchange data. July 1 was the first close below the pre-earnings line; July 2 put the stock 7% under it.

What Micron did during those five sessions is instructive: essentially nothing. The only company items on file are the routine 10-Q, scheduled Form 4s, and a CEO television appearance in which Sanjay Mehrotra told CNBC that customers driving a hard bargain on price had contributed to the shortage and that even customers had failed to forecast the demand they now have. The noise came from elsewhere. TheStreet’s late-Thursday “fresh lawsuit” piece recirculated the antitrust class action that was actually filed June 25 — the suit accusing Micron, Samsung and SK hynix of coordinating DDR4 output cuts, which Micron has denied and says it will fight. Headlines also latched onto Mehrotra selling roughly $46 million of stock on June 26 — sales the Form 4 footnotes show were pre-scheduled under a Rule 10b5-1 plan, though they did execute within days of the all-time high. None of this changed a number in the income statement. All of it changed the price.

The paradox with a name

Here is the uncomfortable part for anyone reaching for the “it’s cheap” argument. At Thursday’s close, Micron trades at 6.8 times forward earnings against 22 times trailing, a $1.1 trillion company priced like a utility with a growth problem. In most sectors that gap screams opportunity. In memory, historically, it screams late-cycle. Peter Lynch put the general rule in writing decades ago: buying a cyclical after years of record earnings, when the P/E has hit a low point, is “a proven method for losing half your money in a short period of time.”

Micron’s own chart is the case study. In May 2018 the stock peaked near $64 while trading at roughly 4.5 times forward earnings — and fell about 57% to $28 by December as DRAM prices rolled over, even though reported earnings were still strong when the slide began. In early 2022 it peaked around $98 at about 11 times forward, then halved by late in the year; fiscal 2023 swung to a $5.8 billion loss. As one memory-cycle retrospective put it this spring: the stock fell 56% “even though earnings were still rising.” The pattern is exactly why Thursday’s sellers do not consider a 6.8x multiple a rebuttal. To them it is the signal — multiples this low appear precisely when the market believes the earnings are peak, not plateau.

What breaks the pattern, if anything does

The bull answer is that this cycle carries structural features no prior one had, and the people making it are specific. Melius Research doubled its target to a Street-high $2,200 after the report, calling memory “the bottleneck of all bottlenecks” in the AI buildout. The June 25 wave of seventeen raises included KeyBanc going from $600 to $1,600 in one step; the most cautious tracked call is Goldman Sachs at $1,100, a Neutral — above Thursday’s close. Across the 45 analysts StockAnalysis.com tracks, the average target is $1,486, the median $1,550, and not one carries a Sell.

The substance behind that conviction: HBM — the high-bandwidth memory that feeds AI accelerators, the toll booth TECHi described in May — is booked solid through calendar 2027, per the June 24 earnings call, with demand conversations reaching into 2028. A growing share of revenue now ships under long-term agreements rather than spot pricing. And Micron’s capital plan — about $27 billion this fiscal year, signaled north of $40 billion next — is not the posture of a management team quietly preparing for a downturn. In 2018, when the cycle cracked, there were no multiyear AI contracts and no customer paying component-inflation surcharges just to stay in the queue. The counter-argument writes itself, though: every cycle’s bulls have an explanation for why the pattern is obsolete, and the 2018 version — data centers would smooth demand forever — sounded equally structural at the time.

How to know which one this is

The signposts are concrete, and none of them require guessing. First, the peer prints land within weeks: Samsung’s preliminary numbers are due around July 7 and SK hynix reports its June quarter in late July — either confirms that memory pricing held through the quarter or shows the first crack. Second, the quarterly DRAM contract-price data: the third-quarter forecasts still point up at a slowing rate, and the distinction between decelerating increases and outright declines is the entire difference between a multiple reset and a cycle top. Third, Micron’s own fiscal fourth-quarter report, expected in late September: the $50 billion guide is now the number the whole memory complex has to cash. And in the near term, Monday, July 6 — the first US session after a violent week that TECHi has covered from the sector side resolved into a Korean rebound while American screens were dark.

The honest framing of Micron at $975 is that the market has already made a call the company’s own numbers do not yet support: that fiscal 2027 estimates are the top of this cycle, not a step on the way up. If the contract structure holds pricing and the $50 billion quarter lands, the round trip of the best quarter in the company’s history will look like the buying opportunity the low multiple advertises. If DRAM prices roll while capex doubles, it will look like May 2018 with bigger numbers — and Lynch’s warning will have aged perfectly, again. The stock spent eight days telling you which way the market leans. The next two earnings prints on the memory calendar will say whether it leaned right.

Investment Disclaimer: This article is for informational and educational purposes only. It is not financial advice and should not be construed as a recommendation to buy, sell, or hold any security. Figures reflect company disclosures, SEC filings, TECHi market data, and public sources available at the time of drafting. Market data may be delayed, cached, or revised. Always conduct your own due diligence and consult a licensed financial advisor before making investment decisions.