Oracle reports on June 10, 2026, and the easy headline is that OCI is finally getting the AI cloud respect it wanted. The better headline is tougher: Oracle is no longer being valued like a late cloud comeback story. It is being underwritten like an AI capacity-financing company.

The June 10 print is not mainly about whether Oracle can say “cloud” louder than AWS, Microsoft Azure or Google Cloud. The market already knows demand is there. Oracle ended Q3 fiscal 2026 with $553 billion of remaining performance obligations, up 325% year over year, and Cloud Infrastructure revenue grew 84% to $4.9 billion. The question now is whether Oracle can build enough capacity to serve that demand without overbuilding, overborrowing or compressing cloud margins.

TECHi’s earnings watch currently lists ORCL for June 10, time TBD, with an EPS estimate of $1.58. That number matters for the calendar, but it should not dominate the setup. Oracle’s own March guidance pointed to Q4 non-GAAP EPS of $1.96 to $2.00 and total cloud revenue growth of 46% to 50% in U.S. dollars. The real earnings-day test is not a one-line EPS surprise. It is the financing model behind Oracle’s ambition to become the landlord for AI compute.

Article Brief

Key takeaways

4 points24s read

- The new frameOracle is not simply a cloud recovery story anymore. The market is pricing whether OCI can become AI infrastructure real estate without taking too much balance-sheet risk.

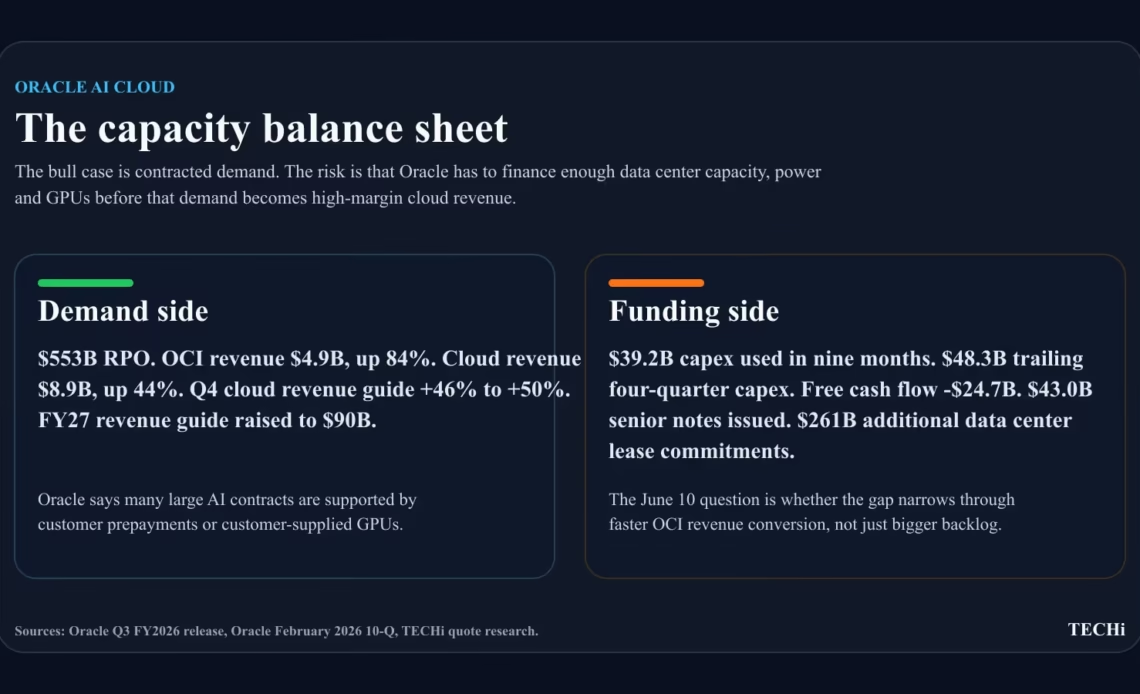

- The demand proofOracle reported $553B of RPO at Q3 FY2026, OCI revenue of $4.9B, and FY2027 revenue guidance of $90B.

- The capital testOracle guided FY2026 capex to $50B, used $39.2B for capex in the first nine months, and disclosed $261B of additional data center lease commitments.

- The investor questionA bullish June 10 print needs RPO conversion, OCI capacity delivery, credible cloud margin and less anxiety around debt, preferred equity and lease commitments.

The AI cloud landlord thesis

The strongest Oracle story is not that legacy database customers are finally moving to the cloud. That was the 2020s version. The 2026 version is more like infrastructure real estate: Oracle signs long-dated AI capacity commitments, builds or leases the data center footprint, secures power and GPUs, and rents the compute layer to customers that need massive AI training and inference capacity now.

That model can be powerful because scarcity creates pricing power. If frontier labs and hyperscalers need clusters before AWS, Azure or Google can supply them, Oracle becomes a capacity broker with real leverage. It also becomes dangerous if demand slows, model-training economics change, customers renegotiate, or Oracle builds capacity faster than it can bill it. In that bear case, today’s backlog becomes tomorrow’s utilization problem.

Oracle knows this is the risk. In its Q3 release, the company said most of the increase in RPO related to large AI contracts where it does not expect to raise incremental funds because equipment is either funded upfront through customer prepayments or supplied by the customer. That sentence is the most important sentence in the whole setup. It tells investors Oracle wants to scale OCI without owning every dollar of GPU risk itself.

Why backlog alone is no longer enough

A $553 billion RPO number is enormous, but RPO is not cash flow. It is a promise to recognize revenue later, subject to contract terms, deployment timing and customer usage. That distinction matters because Oracle is spending ahead of recognition. In the first nine months of fiscal 2026, Oracle used $39.2 billion for capital expenditures, up from $12.1 billion in the comparable fiscal 2025 period. On a trailing four-quarter basis, capital expenditures were $48.25 billion and free cash flow was negative $24.74 billion.

That is not automatically bearish. Data centers are built before they produce revenue, and a capacity-constrained AI market can reward the company willing to build early. But it changes the stock. Investors are no longer just underwriting software margins. They are underwriting construction timing, customer prepayments, power contracts, GPU supply, lease duration and financing cost.

The balance sheet is now part of the product

Oracle raised $30 billion in February through investment-grade bonds and mandatory convertible preferred stock after announcing a broader plan to raise up to $50 billion in debt and equity financing. The February 10-Q shows $43.0 billion of senior notes issued during the first nine months of fiscal 2026, a $5.0 billion mandatory convertible preferred issue, and a $20 billion at-the-market common stock program that had not been used as of February 28.

That funding stack is the price of trying to become the AI cloud landlord. It gives Oracle the cash and market access to build. It also makes interest expense, lease obligations and dilution risk part of the earnings story. TECHi’s financials page flags a debt/equity ratio of 5.20 and interest expense equal to 28.76% of annual net income. Those are not fatal numbers for a company with Oracle’s enterprise software base, but they leave less room for a sloppy buildout.

The 10-Q adds another layer: as of February 28, Oracle had $261 billion of additional lease commitments, substantially all tied to data center arrangements, generally expected to commence between Q4 FY2026 and fiscal 2028 for terms of 15 to 19 years. Those commitments were not yet reflected on the balance sheet. There were also $11 billion of unconditional purchase and other obligations, primarily related to data center power arrangements.

What June 10 has to answer

A routine earnings preview asks whether Oracle beats EPS. This one should ask six harder questions. Did RPO grow, but more importantly, did recognized cloud revenue accelerate? Did capex guidance rise again, and if so, does management explain what demand is funding it? Did cloud and software margins hold despite infrastructure expense? Did customer prepayments and customer-supplied GPUs continue to reduce Oracle’s capital at risk? Did management keep the FY2027 $90 billion revenue guide credible? And did financing commentary reduce, rather than increase, concern about debt and leases?

Tomorrow advice for traders

For short-term traders, ORCL is a cleaner setup if the stock holds strength into the report without becoming a crowded one-day chase. TECHi’s quote page showed Oracle at $214.34 at 9:40 a.m. EDT on May 29, up 5.22% on the session, with a TECHi next-session signal of Hold and an expected +0.9% move. That is constructive, but not a green light to ignore event risk.

The practical trading read is this: before June 10, focus less on the EPS whisper and more on whether the market is rewarding AI capacity names again. A rally into the print that comes with improving sentiment around Dell, Nvidia, Broadcom, data center power and AI infrastructure is healthier than a solo ORCL spike. On earnings day, the first move may be driven by EPS and cloud revenue. The second move will probably be driven by capex guidance, RPO quality and free-cash-flow commentary.

The one-year investor view

For one-year investors, Oracle is investable if the company proves that AI capacity is not just expensive growth. The stock does not need a perfect quarter. It needs evidence that backlog is converting, the cloud business can absorb infrastructure expense, and the financing stack is controlled. That is why June 10 matters. A beat without cleaner capex commentary is not enough. A modest EPS result with strong RPO conversion and disciplined funding could be more important.

Oracle has a real shot at becoming one of the most important landlords in the AI economy. Its advantage is not that it discovered cloud late. It is that it may be willing to finance scarce AI capacity faster than competitors, while using its database franchise and multicloud position to pull customers into OCI. But landlords make money when assets are occupied at good yields. They lose money when they build into the wrong cycle.

That is the entire Oracle earnings preview in one line: OCI backlog is huge, but AI capex is the real test. If June 10 shows capacity turning into revenue and cash, ORCL can keep the AI landlord premium. If it shows another round of bigger spending without a tighter revenue bridge, the market will start asking whether Oracle is building the future or just financing it.

Investment disclaimer: This article is for informational and educational purposes only. It is not financial advice or a recommendation to buy, sell or hold any security. Earnings dates, estimates and market prices can change quickly. Verify current quotes and consult a licensed financial advisor before making investment decisions.